Credit Card Loan Balances at Big 4 Banks kept growing in 2023

Total unpaid credit card balance reached a new record high last year. Delinquency rates have surpassed their pre-pandemic highs. Yet banks' executives are confident there is no cause for concern.

Photo: Nick Sarvari/Unsplash

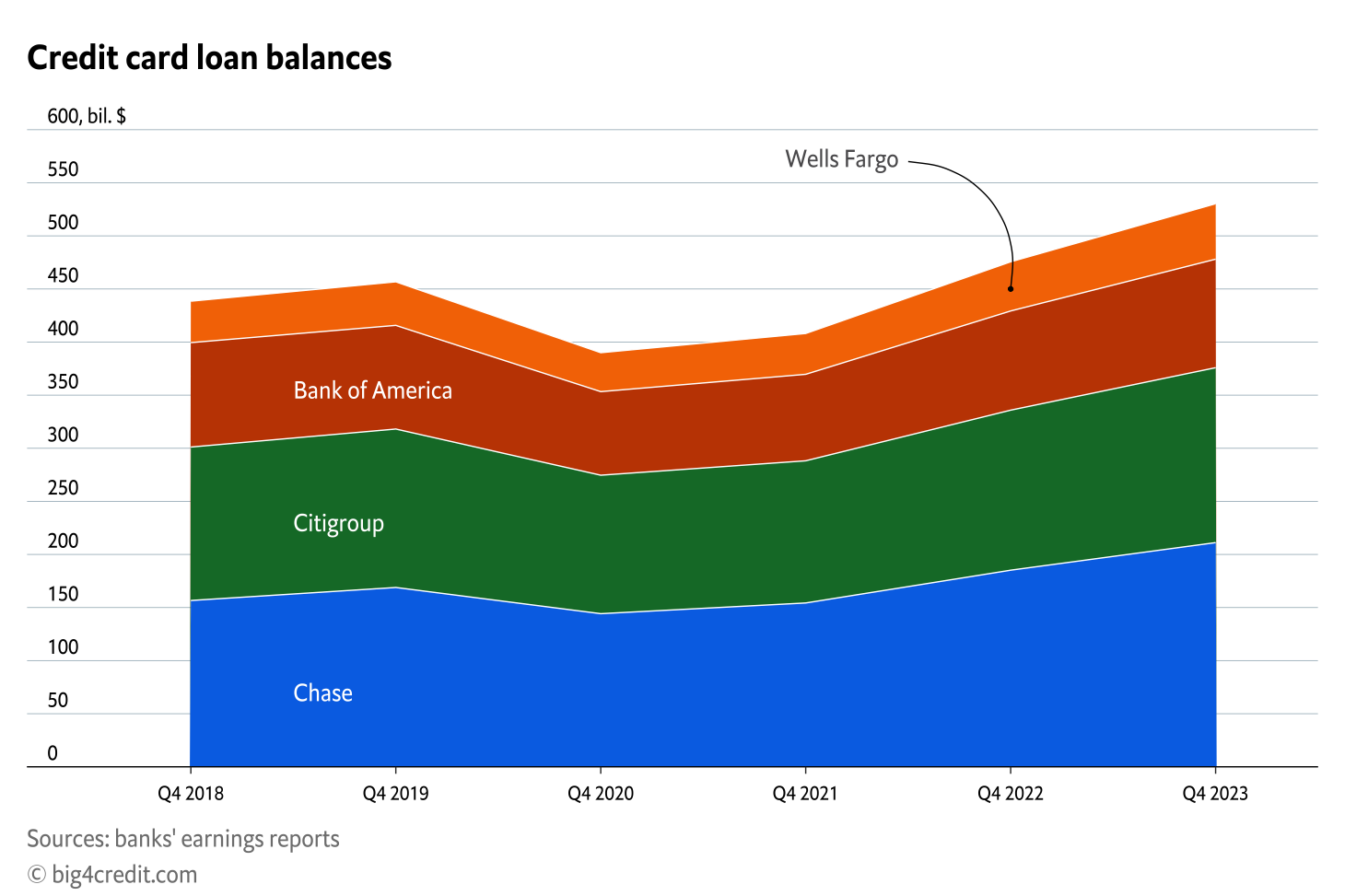

The total credit card balance of the U.S. major banks - JPMorgan Chase, Bank of America, Citibank, and Wells Fargo - rose 11.5% over 2023 and reached a new record high of 530.31 billion dollars. JPMorgan Chase and Wells Fargo have demonstrated the largest increases in their credit card loan portfolios, with 14% and 12.8%, respectively, compared with 2022. Credit card loans at Bank of America rose 9.3%, while Citibank climbed 9.4%.

Big 4 bank ended Q4 2023 with the unpaid credit card balances as follows,

- JPMorgan Chase - $211.18 billion

- Citibank - $164.7 billion

- Bank of America - $102.2 billion

- Wells Fargo - $52.23 billion

In spite of hitting a new record value, the total credit card debt at Big 4 banks grew at a relatively moderate rate in 2023 than a year earlier when it reached 16.5%.

Consumer savings, which swelled during the pandemic, finally began to dwindle, leaving consumers with less money to spend. In 2023, total consumer deposits declined at all four banks. Wells Fargo saw the largest outflow in consumer deposits which declined by 9%. Deposits at Bank of America and Citibank both fell by 8%. JPMorgan Chase ended the year with a 3% drop in deposits compared to 2022.

Even as the inflation rate has significantly slowed, high prices on everything from food to housing push consumers to take up more credit card debt. For banks, however, growing unpaid credit card balances combined with the highest interest rates in the decade would imply bigger revenue and net income. Big banks typically pay very little on consumer savings and don’t increase their savings APR as federal funds rate goes up.

Yet, bank executives are not worried about consumers’ health right now. The latest data suggest that the economy is on track for the so-called ‘soft landing.’ It is possible that in this economic cycle the Fed’s policymakers would be able to avoid tumbling the economy into recession while keeping the inflation rate low and the labor market strong. “And a very strong labor market means, all else equal, strong consumer credit,” says Jeremy Barnum, JPMorgan Chief Financial Officer, during the Q4 2023 earnings call.

With pandemic relief measures, e.g., stimulus checks, more generous unemployment insurance, student loan payment pause, and others ending in 2023, customers started to feel more financial stress than during the pandemic years.

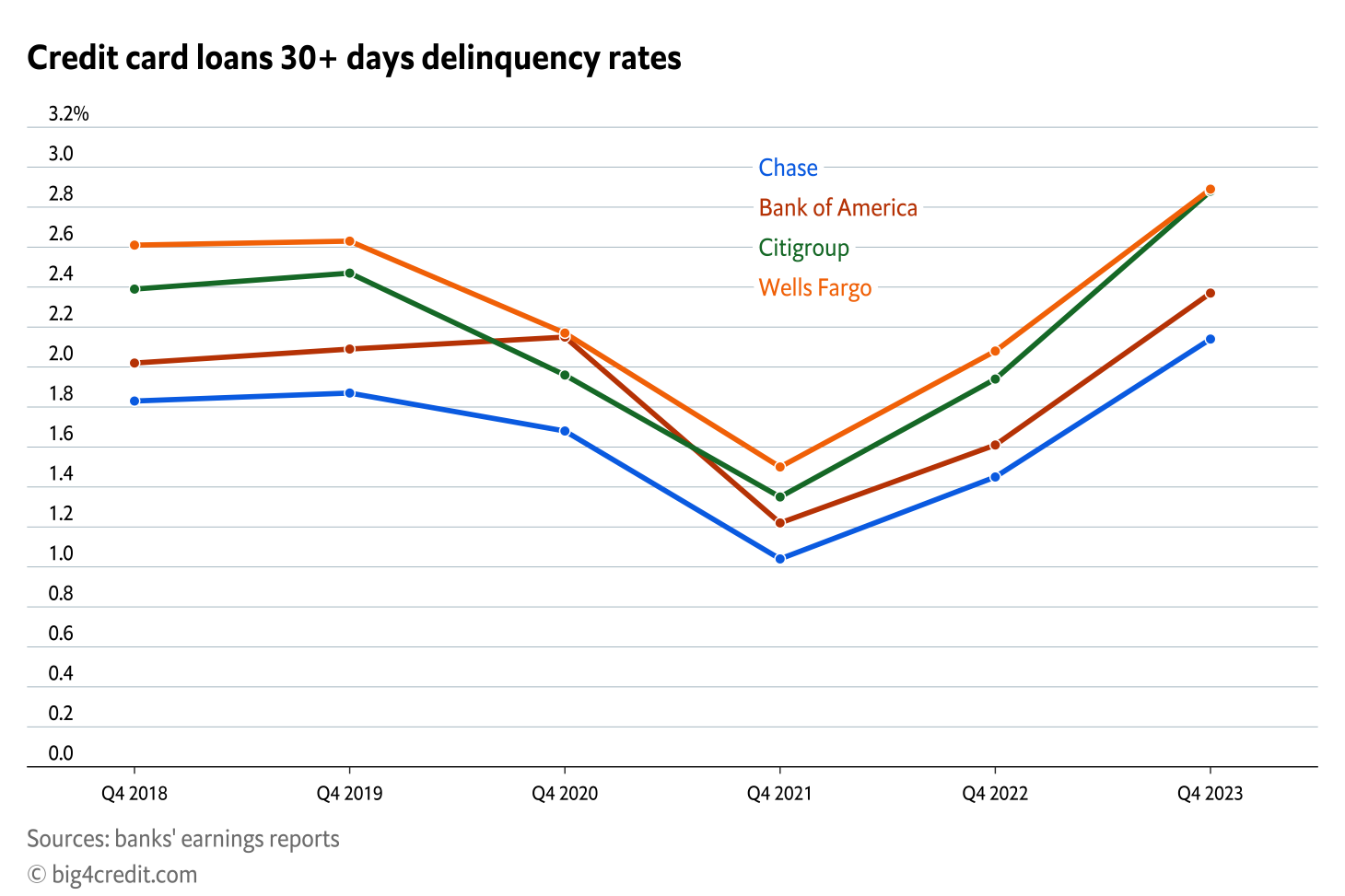

Delinquency rates at all four banks jumped in 2023 and surpassed the pre-pandemic levels. Higher delinquency rates mean that borrowers are struggling to meet their debt payments.

Citibank and Wells Fargo ended Q4 2023 with a 30+ days delinquency rate of 2.9%. JPMorgan Chase and Bank of America had 2.1% and 2.4% respectively. Even though the unpaid credit card balances for most banks except Bank of America surpassed the pre-pandemic level in 2022, the delinquency rates remained low. Last year, despite a strong labor market and improved inflation rates, U.S. consumers showed that their financial health had worsened, as indicated by the elevated delinquency rates at all four banks.

Credit card 30+ days delinquency rates for Big 4 banks in Q4 2023 were as follows,

- JPMorgan Chase - 2.1%

- Citibank - 2.9%

- Bank of America - 2.4%

- Wells Fargo - 2.9%

“In terms of the consumer resilience (…). The way we see it, the consumer is fine,” said Jeremy Barnum.

By all accounts, 2023 has been a challenging year: it had natural disasters and geopolitical tensions, started with some of the largest bank failures in the U.S., experienced the fastest interest rate increases in history. Most economists also predicted economic recesssion within a year.

“Instead, 2023 showcased economic resilience led by U.S. consumers despite higher interest rates.”, said Brian Moynihan, Bank of America Chief Executive Officer, during the earnings call for the period ending December 31, 2023.