Rent a Car, Skip the Extra Insurance — Your Credit Card Has You Covered

Credit card auto rental insurance can save you money and give you peace of mind. Here's how to check if your card offers this benefit, how to use it when renting a car, and which cards provide the best coverage.

Photo: Big4Credit

When renting a car, you’re often offered additional insurance at the rental counter. Before accepting this extra expense, check if your credit card already provides rental car insurance. Many credit cards include this benefit, which can save you money and offer valuable protection. This article will explain how credit card rental insurance works, how to check if your card offers it, and how to use it effectively.

Auto Rental Insurance: Key Terminology

Credit Card Rental Insurance: This broad term refers to any insurance coverage provided by your credit card when renting a car. It includes various protections, such as Collision Damage Waiver (CDW) and Loss Damage Waiver (LDW). Coverage can be primary (paying first before your personal insurance) or secondary (paying after your personal insurance has covered costs).

Auto Rental Collision Damage Waiver (CDW): This coverage helps pay for damage to the rental car resulting from an accident or theft. It typically covers repair costs or the vehicle’s actual cash value. CDW is a common benefit included in credit card rental insurance but is just one type of coverage.

Loss Damage Waiver (LDW): This typically includes CDW but also covers the loss-of-use charges, administrative fees, and sometimes personal property loss. It is often bundled with CDW but can be distinct in some policies.

Check Your Card’s Rental Car Coverage

Many people aren’t aware that their credit cards offer rental car insurance. This benefit is often included with travel rewards cards but isn’t always well-publicized. As a result, some cardholders might end up buying extra rental car insurance at the counter because they don’t know their card already provides coverage. To help you avoid unnecessary insurance costs, here’s a simple way to check if your credit card includes rental car coverage:

Review the Benefits Guide: Check the benefits guide or user agreement that came with your credit card. This document lists all the benefits, including any car rental insurance. You can also usually find it by logging into your online bank account or through your credit card issuer’s app.

Visit the Issuer’s Website: Go to your credit card issuer’s website and look for the benefits or rewards section. Information about car rental insurance and other perks is usually available there.

Call Your Bank’s Customer Service: Reach out to your credit card issuer’s customer service team. They can confirm whether your card includes car rental coverage and provide details about the insurance.

Getting More Information From Your Bank

- Chase: Information about car rental coverage is available through your account on the Chase website or app under the “Credit Card Benefits” section within the travel category.

- Wells Fargo: All Wells Fargo cards include Auto Rental Collision Damage Waiver. You can view and download the Benefits Guide for each card on the Wells Fargo website.

- Bank of America: Car rental coverage details may not be readily visible online. It’s best to call their Benefits Team at 1-800-592-4089 for information or to request a physical copy of your Credit Card Benefits Guide.

- Capital One: You can download the Benefits Guide for car rental coverage from the Capital One Benefits website. Make sure to select your credit card type (e.g. Visa Signature, Visa Infinite, World Mastercard, World Elite Mastercard).

- American Express: Many cards provide secondary coverage, and there’s an option to purchase Premium Car Rental Protection for primary coverage. To check if your card includes Car Rental Loss and Damage Insurance and to view the Benefits Guide, click the link and select your card: American Express Benefits. For additional questions, contact customer service at 1-800-338-1670.

- Citi: Some Citi cards may include car rental insurance. Check your card benefits on the Citi Card Benefits website or call customer service at 1-800-950-5114.

Understanding Your Card’s Rental Car Insurance

Understanding how credit card rental car insurance in details is essential for maximizing this benefit and ensuring you’re protected while renting a vehicle.

Coverage Overview

What’s Covered: This typically includes damage to the rental vehicle caused by an accident or theft. You will be reimbursed up to the maximum coverage limit for either the repair cost or the vehicle’s actual cash value, whichever is less. Some credit cards may also cover additional costs such as:

- Loss-of-Use Charges: Fees charged by the rental company for the time the vehicle is out of service for repairs.

- Reasonable Towing Charges: Costs to tow the vehicle to the nearest repair facility.

- Administrative fees or taxes: Additional fees imposed by the rental company..

What’s Not Covered: The Collision Damage Waiver (CDW) benefit does not cover everything. Specifically, it does not include:

- Damage to Other Vehicles: Coverage does not apply if you damage another driver’s car.

- Injuries: Injuries to you, your passengers, or others are not covered.

- Third-Party Property Damage: Damage to fences, buildings, or other property is excluded.

- Personal Belongings: Loss or theft of personal items inside the rental car is not covered.

Primary vs. Secondary Coverage

Primary Coverage: This means the credit card insurance covers damages first, without requiring you to claim through your personal auto insurance.

Secondary Coverage: This type of insurance kicks in only after your personal auto insurance has paid out. If you don’t have personal insurance, this coverage acts as primary. Note that outside the U.S., secondary coverage is typically treated as primary.

Exclusions and Limitations

Coverage Limits: Typically range from $50,000 to $75,000, but limits can vary by card issuer and card type.

Rental Periods: Generally, rental car insurance covers rentals for up to 31 consecutive days.

Geographic Limitations: Coverage usually applies in the U.S. and most international locations but excludes countries such as Israel, Jamaica, the Republic of Ireland, and Northern Ireland.

Common Exclusions: Certain types of vehicles are often excluded from coverage, including:

- Expensive Cars: High-end brands like Ferrari, Lamborghini, and Rolls Royce.

- Antique Vehicles: Cars older than 20 years or not manufactured in the last 10 years.

- Vans: Typically not covered, except for small-group vans with up to 9 seats.

- Special Vehicles: Trucks, motorcycles, RVs, and vehicles with open cargo beds.

- Vehicles Rented with a Driver: Coverage does not apply if the vehicle is rented with a driver.

Two Key Parts of Credit Card Rental Insurance

There are two major aspects of your credit card auto rental insurance: Coverage Activation and Filing a Claim. Without an active coverage, your rental car is not protected and you will not able to file a claim.

Coverage Activation

Make sure you have activated your coverage before hitting the road with your newly-rented car .

Firstly, ensure the following conditions are met,

Cardholder Name: You must be the primary cardholder and the primary driver. Coverage applies to you and any additional drivers listed on the rental agreement.

Payment Requirement: You must pay the full cost of the rental car with the covered card. This includes using the card for both the initial reservation and the payment at the rental counter.

Secondly, when going through the rental agreement paperwork, don’t sign up for any insurance coverage from the rental agency,

Decline the Rental Company’s Insurance: You must decline the rental company’s insurance. Accepting this additional insurance generally cancels out your credit card coverage.

These two simple steps will ensure you’re protected while renting a vehicle!

But Don’t Leave Just Yet, Inspect Your Rental Car

Before leaving the rental lot, a wise renter does the following,

- Check for Existing Damage: Carefully inspect the rental car for any pre-existing damage, such as scratches or dents, on both the interior and exterior.

- Report Any Damage: If you discover any damage, immediately report it to the rental company. This ensures that the damage is documented, protecting you from being held responsible for it later.

- Get a Confirmation from rental agency : Ensure that the rental company notes the damage in your rental agreement and/or provides you with a written record. This documentation will help you avoid potential disputes when returning the vehicle.

Filing a Claim

To file a claim, you typically need to do these crucial steps,

Gather Required Documents:

- Accident Report Form: Obtain and include a copy of the report detailing the incident.

- Rental Agreement: Provide proof of the rental contract.

- Repair Estimate and Bill: Submit copies of the repair estimate and itemized bill for the damages.

- Photographs: Include two or more photos of the damaged vehicle, if possible.

- Police Report: If applicable, provide a copy of the police report, especially for accidents or theft. If a police report is not available, indicate this in your claim.

- Demand Letter: This is typically required to detail the total costs and amounts covered by other sources. However, its necessity can vary based on your specific situation and the card issuer’s policies.

Report the Incident to the Benefit Administrator: Notify the Benefit Administrator of the damage or theft as soon as possible. Prompt reporting is crucial to ensure your claim is processed efficiently and to avoid potential delays or denial.

Submit Your Claim:

- Completed and Signed Claim Form: Fill out and sign the claim form as required.

- Credit Card Statement: Provide a statement showing the last four digits of your account number and confirming that the entire rental transaction was paid with the covered credit card.

- Additional Documentation: Include any additional documents requested by the Benefit Administrator to support your claim.

Rental Car Company Won’t Accept Your Credit Card Insurance?

Beware that rental agencies often promote their own insurance and coverage options as it’s a significant revenue stream for them. This can sometimes lead to staff being especially insistent on purchasing their insurance products, driven by commission structures or company policies.

Here’s the key: if your credit card provides rental car insurance, the rental agency must accept it as long as it meets the required conditions. Understanding your credit card benefits and their terms is crucial.

If you encounter resistance from the rental company or they insist on you buying their insurance, don’t hesitate to reach out to your credit card’s Benefits Administrator. They can verify your coverage and provide advice on how to handle the situation with the rental agency.

For international rentals or certain rental companies, you might need a letter of coverage from your credit card issuer to confirm your insurance. Here’s how to get it for some popular credit cards:

Chase: Request a letter of coverage by calling 1-800-349-2634 or visiting the new Chase benefit provider website.

Wells Fargo: Call 1-800-316-8051 or visit the Wells Fargo benefit provider website to request a letter of coverage.

Request Proof of Rental Car Coverage in Advance

Requesting a letter of coverage in advance will save you from any possible headache when renting a car from the agency.

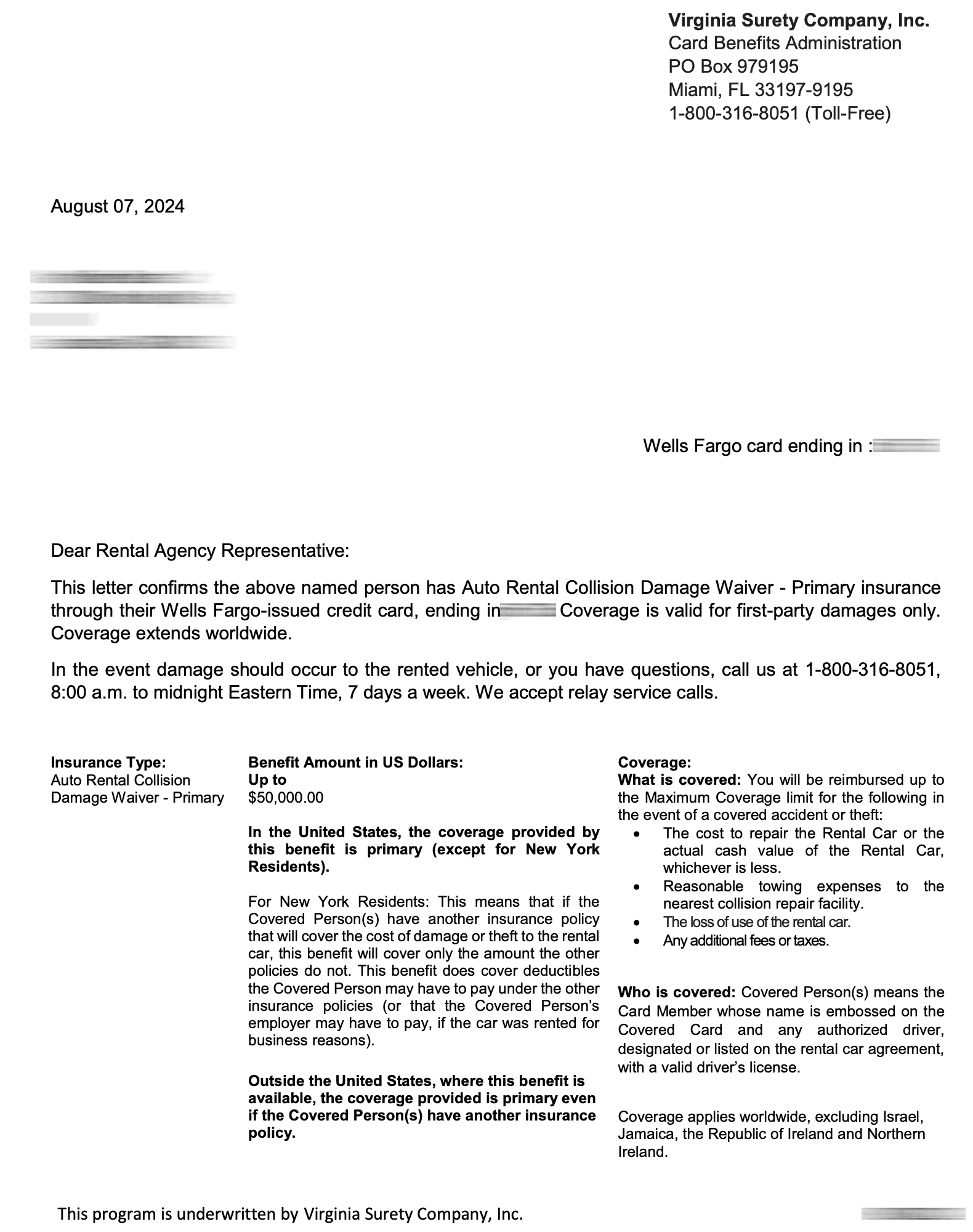

Wondering what a coverage letter actually looks like? Here’s a real example from Bilt Mastercard,

Letter of Coverage is underwritten by Assurant through the Bilt Mastercard

A similar Letter of Coverage for most Wells Fargo credit cards can be requested at https://mycardbenefits.assurant.com/, and it will be sent to you via email within 5 minutes.

No Credit Card with Auto Insurance Benefit? Try These Cards

If you’ve checked your credit cards and found that none offer rental car insurance, it might be worth considering a new card with this benefit. Many credit cards with rental insurance offer secondary coverage, but premium cards often provide primary coverage.

These premium cards usually come with an annual fee but offer additional valuable travel benefits. For example, Chase Sapphire Reserve and Chase Sapphire Preferred cards, all include primary rental car insurance along with other perks.

If you prefer a card with no annual fee but still want primary coverage, Wells Fargo One Key® offers primary rental car insurance at no annual fee. If you’re looking for even more card options, check out our guide to the Best Credit Cards With Auto Rental Insurance.

Disclosure: The information about credit card rental insurance in this article has been independently researched and compiled by big4credit.com. The details and card benefits described in this article have not been reviewed, approved, or endorsed by any credit card issuer. Always verify with your card issuer for the most accurate and up-to-date information.